Busting Common Crypto Narratives and Myths

The crypto community often embraces a libertarian view of economics that can be traced back to the Austrian school of economic thought. At Aaro Capital, though we hold a similar view on the evolution and potential of this asset class, we derive our reasoning from established economic thinking. We are convinced of the need to embrace modern economic thought, which has been built on competition of ideas, internally consistent economic models, and rigorous analysis of real-world data. We also believe in the progress of technology, and ultimately aim to exploit investment opportunities that can capture the value that is generated from it.

In this article, we first define economics as a data driven social science, something which is often overlooked by many who cherry pick economic arguments and observations to support their personal views. We then describe how a more evidence-based and modern economic approach supports or qualifies key beliefs and arguments about crypto.

Economics as a Data Driven Social Science

Economics has built itself as a data driven social science. However, differently from natural sciences, economists can only do limited experimentation to test theories and produce new data. This is especially the case for macroeconomics and finance. Moreover, economics is a social science studying a particular complex and self-interacting system in which the very expectations of the subject of the study can determine the outcome.

Given the complexity of the economy in the real world, and the lack of reproducible experimental data, often economists consider many theories and models with legitimate claims of matching the data. Therefore, statistical inference in economics (as in epidemiology) is very important. In such complex environments, causal relationships on a macro level are extremely difficult to discern, with economic phenomena being the outcome of complex webs of interconnected effects and countereffects.

On the one extreme, statistical inference is not deemed important when experimental data can decisively and progressively rule out theory that does not fit the data to the degree of precision required. This is the case of many natural sciences. On the other extreme, statistical inference is of no use when there is no way in which they can distinguish decisively among theories. This is the case with philosophy. Economics sits somewhere in between where formal statistical inference can help in testing hypotheses against real world data and allowing for reasonable choices of theories using notions of probability, to sharpen our knowledge of the world and to pragmatically inform policy decisions.

This modern view of economics as an empirical science sets it apart from older views of economics being a form of speculative thinking, heavily influenced by political views and opinions. At Aaro Capital, we embrace a humbler view of economics as a data driven science and are little interested in more grand political driven visions.

Bitcoin, Gold and the Store of Value

The first narrative to qualify is the digital gold / store of value / inflation hedge narrative, which is based on the Austrian school of economic thought and most commonly linked to bitcoin. The general background behind this thinking is that Austrian economists were very critical of the concept of fiat money. Along their line of attack, many in the crypto space claim that central banks and fractional reserve banking are the primary source of business cycle fluctuations in the economy. Governments have a persistent temptation of increasing the money supply to finance spending and subsequently generate inflation that "steals" people's wealth. This is a key point of Hayek’s critique of government monopoly over the issuance of money.1

The thinking implies that cryptocurrencies can create a new “gold standard”, offering new forms of hard currency. As Bitcoin has a fixed and inelastic supply curve, which cannot be debased, the idea is that it is an inherently a better form of money than modern fiat currency.

In practice, however, most economists would agree that the gold standard or anything like it is a bad idea. If money supply is fixed, determined by the supply of gold or bitcoin, it cannot adjust in response to changing economic conditions. Hence money cannot be used to smooth out external economic shocks, such as the COVID-19 shock on the economy. If all economic shocks are fully reflected in the real economy, prices can be very volatile in the short term. In the medium and long run, a growing economy priced against a nearly fixed supply of gold or bitcoin would experience deflation.

Is this a good property for money, as many would claim in the crypto world?

The answer is no. Much of what modern economics covers on economic fluctuations can be condensed into New Keynesian macro models. These are the workhorse models of modern central banks and do a relatively good job at matching historical data. In these models, when prices and wages are sticky, and particularly when it is harder to adjust prices downwards rather than upwards, using a form of money which is fixed in supply and deflationary results in worse outcomes than a low inflationary currency with a flexible supply, i.e. one that can respond appropriately to economic shocks.2

Would global adoption of bitcoin as a universal currency make sense?

The answer is no. It would be the same situation as when all countries followed the gold standard and were forced to maintain fixed exchange rates. Flexible exchange rates are important as they can efficiently absorb international economic shocks. Without flexible exchange rates, all shocks must hit the real economy, which can cause painful downward price adjustments. The economic fallout of downward price adjustments can be seen in European periphery countries in the 2010s or the old industrial heartlands in the UK's industrial north or the US's rust belt. In fact, there is little macroeconomic support for bitcoin becoming the global reserve currency.

Does this imply that central banks are therefore the main source of macroeconomic instability?

The answer is yes, but only in already unstable countries. Even there, the instability lies in unsound fiscal policies and central banks that lack independence. Independent and credible central banks have been effective in maintaining stable prices in advanced economies, even during the 2008 Financial Crisis and Great Recession.

Track records of central banks are more mixed in emerging economies, where independence is often challenged by political interference, weaker institutions and more precarious macroeconomic management practices. These challenges are reflected in volatile emerging market currencies, high rates of inflation, and occasional bouts of hyperinflation that debase the value of currencies, for example in Venezuela and Zimbabwe. Those cases remind us of the Austrian critique of public money and why private monies can be superior in countries where there are weak institutions.

However, for advanced economies, economic research has firmly shown that most of the observed variation in monetary policy instruments, such as interest rates and monetary aggregates, is due to central banks reacting to economic shocks to stabilise the prices and growth.3 This undermines the claim that modern monetary policy is the main source of business cycle fluctuations.

Again, our thinking is that progress lies ahead. Battle-tested mainstream economics, however incomplete and imperfect as it may currently be, is better than trying to reinvent the economic wheels. The Austrian school of economics has indeed provided important contributions to modern economic thinking, but many of its conclusions are generally not supported by the economic evidence, unless one cherry picks historical data. So far, the Austrian economists have not been able to produce a macroeconomic model which is able to do a reasonable job matching historical data as a whole.

Inflation vs Asset Appreciation

The argument surrounding the store of value function of bitcoin and other cryptocurrencies is often connected to views on how unconventional monetary policy may debase the value of the dollar or other fiat currencies, as well as expectations about inflation.

The Fed, the ECB, Bank of England, and other leading central banks used quantitative easing to stimulate the economy after the financial crisis. Quantitative easing involves central banks buying government bonds in the secondary markets to push prices up and yields down to ease financial conditions. In the crypto community, this is seen as a dangerous tool that can lead to debasing of a fiat currency.

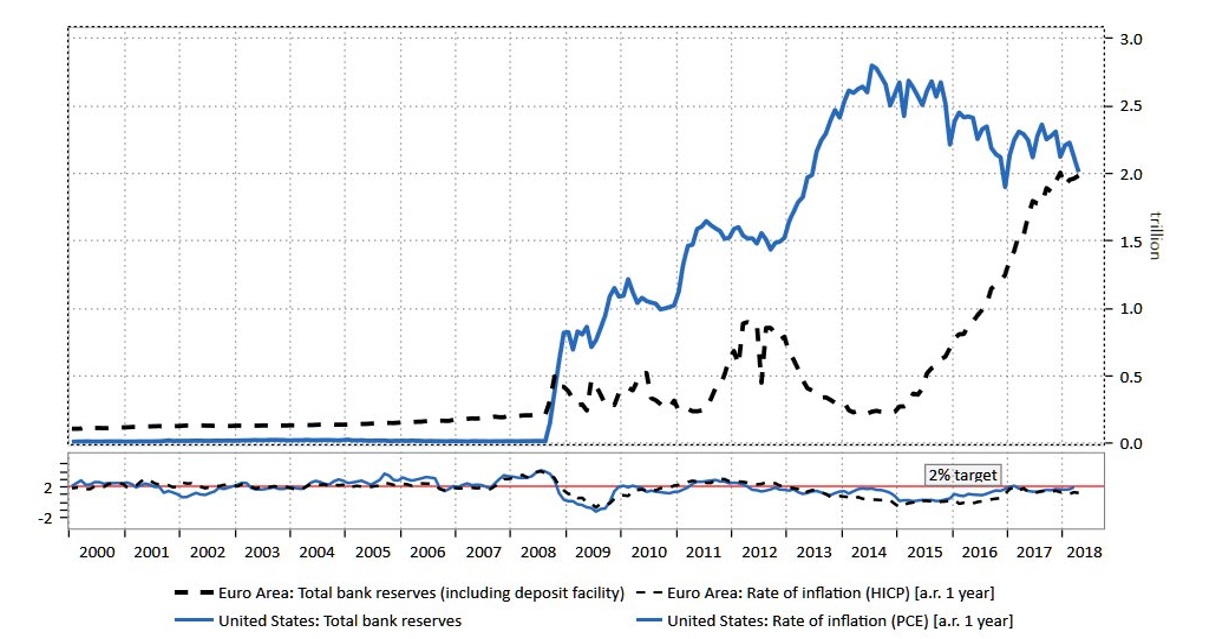

Figure 1: Size of the central bank reserves and inflation rates for the US and the Euro Area

We are not convinced by this line of thought. Economic theory tells us that when the need for liquidity is saturated and hence additional liquidity has no effect on the liquidity premia, then an increase in the size of the central bank balance sheet has no effect on inflation if interest rates (and expectations of future interest rates) remain unchanged. This has been confirmed by the fact that, despite large increases in central bank balance sheets, inflation has remained low over the last 10 years in the US and in the Euro Area (see Figure 1). Of course, we agree that if governments start monetising their debts, then inflation and inflation expectations should go up, but that is another story.

Saying that, we acknowledge that inflation is hard to forecast and that the large fiscal expansion during the COVID pandemic in many advanced economies creates tail risk for fiscal stability and hence inflation. These risks are relevant to any investor because, if materialised, they can erode returns in real terms.

Are central banks slowly inflating away the value of fiat currencies?

It is true, as some notice in the crypto community, that central banks in advanced economies target a positive inflation rate, and hence nominal prices in the economy go up over time. Yet, a low and stable level of inflation rate guarantees that all legal contracts, for example loan contracts, wage contracts or service provider contracts, can factor in the expected price path without either consumers or investors suffering losses in real terms. This expected inflation is taken into consideration when negotiating interest on loans or setting the price of bonds and risky assets such as stocks and property. Investors only hold depreciating cash for liquidity and invest in appreciating or income generating assets to grow their wealth. Therefore, low and predictable levels of inflation have little effect on the real economy and only deviations from expected inflation redistribute wealth.

At the same time, a small positive inflation rate can offer space to central banks when setting policy, for example in the case of a recession (and maybe even does not provide enough space for monetary policy, as the current zero interest rates have shown). This allows them to better manage and smooth business cycles. Indeed, with inflation low, stable, and mostly on target at least since the mid-80s, central banks in advanced economies have a good track record to show.

Are bitcoin and other cryptoassets an inflation hedge?

Most investors would agree that they are not. Yet, many in the crypto world often confuse high returns (that should always be adjusted for risk) with “inflation hedge” properties. To be an inflation hedge, an asset must correlate with unexpected changes in inflation, i.e. inflation surprises. However, cryptoassets appear to have very low correlation with inflation surprises.4 Our rationale is that one should invest in this market to harness high risk-adjusted returns and to diversify portfolios.

A different argument often heard in the crypto community is that the Consumer Price Index (CPI) is somehow a misleading measure of inflation, due to the difficulty in measuring a basket of goods for the “representative consumer”. For example, if you are a wealthy investor, then your rate of inflation should include assets and services you want to acquire – university education, real estate and other asset prices. Some of these assets had large price increases over the last few years. The increases in prices may be as high as 20%, or even higher. But this argument does not make sense from a modern economics perspective.

First, it is true that CPI is a statistical construct that may capture more or less of one individual’s pattern of consumption. It is also true that price indices for individual categories of goods or services have different properties and may correlate more or less strongly. None of them though have yet showed signs of de-anchoring, despite post-COVID pent-up demand and bottlenecks. Importantly, housing is included in CPI but either as a consumption good (rent) or has estimated “owner’s equivalent rent”. Including real estate as an investment asset, or any other asset price, would mix consumption and investment purposes, and importantly inflation vs asset appreciation. Unlike consumption, where goods and services are used purely to enjoy them, investments are made to earn future income. Given the risks involved in investments relative to just holding cash, holding an investment asset must have a greater return than just holding cash, meaning long term investment assets such as stocks or real estate should increase in value over time in a healthy economy. This is very different to consumption goods increasing in value over time, i.e. deflation, due to economic problems or the debasement of the local currency.

Second, it is true that an increase in liquidity, caused by the quantitative easing, could fuel asset price bubbles. With many asset prices going up, we see this risk clearly. For example, the decoupling of the US stock market from macroeconomic conditions may be a signal of that. That is a concern for financial stability (as the pre-2008 housing market bubble shows), but also a concern for investors that need to diversify their risks with an eye on systemic risks as well.

Finally, to look at the very top of the market for real estate or consumption goods (a yacht price maybe?!) to define one’s own inflation rate, is a strange exercise. We believe in sound benchmarks to measure investment returns, regardless of whether the focus is the traditional or crypto space.

Currency Competition

Another recurrent argument in the crypto community is that bitcoin and cryptocurrencies can bring central banks to their knees and end their monopoly on the issuance of money. They would then be substituted by a “market for monies”, in line with Hayek’s liberaltarian idea, where private entities would be allowed to issue non-interest-bearing certificates, competing in an open market for currencies. Only currencies offering a superior store of value would then survive market competition.

Yet, would a world in which only private money existed be a better world?

We think that it would not be the case, at least for a while. However, currency competition between state-money and cryptoassets is indeed a force for good. Let us explain why.

Looking at the data, we note that the Austrian argument for private money does not match up with the historical experience. In the past, private money not backed by a fiscal authority has universally failed in providing stable value to the users. For example, the US free banking era, in 1837 to 1883. Economic theory tells us that the weakness of private money is due to the intrinsic dynamic instability of privately issued currency. When trust in the stability of its value evaporates, lacking a backer of last resort to help support confidence, it suddenly loses transaction value.5

However, the future is likely to see healthy competition between means of payment and between currencies. We believe that market forces and Distributed Ledger Technology will allow money and payment platforms to offer better value for customers and smoother transactions.6

In a digital environment, where each currency and price can be instantaneously converted, switching costs between different currencies are much lower. This provides full convertibility among monies. This enables a key benefit: the store of value and medium of exchange role of money can be "unbundled" and consumers and investors can smoothly choose between state and private money for each function.7

Cryptoassets can transform the currency space and challenge the monopoly of governments over money and the role of money as a public good. This is already happening with central banks around the world planning and introducing Central Bank Digital Currencies (CBDCs).8

These innovations have large transformative potential. Digital monies in the form of global stablecoins have the potential to reshape networks beyond traditional national borders to create new “digital currency areas”, connected via platforms and using given unit of accounts specific to them. However, this could create new barriers to exchange due to network externalities, where users are “captured” on a platform and unit of accounts. Also, economic theories and empirical evidence tells us that there are limits to the size of an optimal currency area. To be efficient, within a single currency area there needs to be labour and capital mobility, economic transfers (i.e. taxation and government benefits) and synchronised business cycles. Digital currencies areas are unlikely to fulfil these parameters and hence could distort economic outcomes.

An important point is that whatever may happen with CBDCs and global stablecoins, the role of cryptoassets in general will not change. They fulfil a different purpose.

DLT and Decentralisation

The big promise of DLT and cryptoassets are the benefits of decentralisation. The more libertarian and anarchist in the crypto community aim for decentralisation due to an anti-government and anti-institution ideology, driven by concerns around perverse incentives of centralised entities and free market thinking. Also, this idea arks back to the Austrian free market stance, and posit that DLT enables a radical decentralisation of not just monies but also the financial system, production networks, social networks and even the functions of the state. This is taking the idea of capitalism further than previously possible. The dream of a free, self-governing society and market using trusted decentralised ledgers and platforms, without the need for controlling and untrustworthy governments, is just around the corner.

At Aaro Capital, we agree that DLT allows for decentralisation for many economic and social players and, in many circumstances, this can achieve better outcomes than centralised entities in many circumstances. In general, where markets can achieve efficient outcomes, the centralisation of economic activity within companies generally allows for greater efficiency, but where markets struggle to achieve efficient outcomes due to market failures, decentralisation of economic activity can achieve better outcomes than government intervention alone in problem markets.

Decentralisation of control enables DLT to solve three fundamental economic issues:

- The disintermediation of trusted intermediaries, helping to cut out expensive middlemen who may also gain excessive market power. Think of how transformative this will be in the financial sector.

- The disintermediation of the hold-up problem, enabling multiple companies to undertake investments together more confidently in mutually beneficial projects, without fearing that the “rules of the game” could be changed unilaterally by a network owner. Granular reorganisation of innovation and production network around DLT is already happening.

- The disintermediation of network monopolies, providing a potential solution to the competition concerns regulators and legislators globally have around the tech giants, who benefit massively from the network effects of their platforms. The shared ownership of the network can also generate a virtuous cycle of growth, using tokens to incentivise participation and contribution to the network.

More broadly, in certain situations, decentralisation enables increased efficiency by removing intermediation costs and lowering barrier to the access to services as well as potentially greater transparency and control over data sharing, reducing the need for government intervention in these problem markets.

But does this transformation allow for a world free of governments?

Certainly not. Sound economic theory tells us that a truly free market can only achieve a remotely efficient outcome under the strict assumptions of perfect competition, where market forces result in the best possible social outcome. The real world violates these strict assumptions in many ways. Market failures, imperfect competition and imperfect information all cause markets to lead to sub-optimal outcomes for society. For centralised firms, the effects of market power, however gained, adversely biases the outcomes towards what is best for centralised firms and not what is best for society overall.

In the real world, given the severity and number of market failures, the only way to achieve a more efficient market outcome is through a government or regulator creating a set of rules for markets and enforcing them. Competition along certain dimensions are good, such as price, quality and variety, but other forms of competition are bad, for example shootouts by drug gangs competing for territory or customers being overcharged by their bank because the terms and conditions were not clear enough for most people to understand. Government and regulators are hence an unavoidable truth for markets and the lesser evil.

This is also true in the crypto space. At Aaro Capital we welcome regulation. Regulators must strike a difficult balance between fostering the benefits of Innovation with other regulatory objectives, managing the risks that come along with It. Without adequate regulation, when things go wrong, this technology, as with anything, could potentially damage consumers, investors and even the wider economy. These risks will prevent many individuals and companies from entering the space, until regulators have provided sufficient clarity around safeguards and regulatory frameworks allowing for trust in cryptoassets. Providing investors and consumers with legal protection can expand the market and thus increase the ultimate value of cryptoassets.9

Conclusion

At Aaro Capital, we believe in investments that support innovation and technological change, in the interest of investors and the society. Our view of the crypto space is forward looking and its benefits and value add are strongly supported by sound and modern economic thinking. We therefore hold a surprisingly similar view on the evolution and potential of the crypto world, relative to crypto and Austrian based narratives, but arrive at our conclusions using a more robust and evidenced based approach.

While the initial idea behind cryptocurrencies was digital cash, the evolution of the technology in second and third generation crypto platforms now enable something far more powerful, Web 3.0. Crypto is a next-generation, value-based internet. As HTTP and HTML are the platform of the World Wide Web, Ethereum and other crypto networks are the platforms of Web 3.0. Web 3.0 is the integration of Industrial Revolution 4.0 technologies and native value management into the internet. So far, the financial payment rails have been kept separate from the Web, but in a digital world where data, money and value are so intertwined, this separation makes less and less sense. Unlocking this potential value revolves around data sharing and flow. The new Web 3.0 business models and infrastructure stack are inherently better at achieving this data integration than the current Web 2.0 business models and infrastructure stack, due to decentralisation enabled via DLT.

Looking at the bigger picture, DLT and cryptoassets are key to the Fourth Industrial Revolution and its use cases are intertwined with technologies such as the Internet of Things, Big Data and Artificial Intelligence. While DLT is the technological Innovation, cryptoassets the economic innovation and they go hand in hand. DLT and cryptoassets have the potential to disrupt virtually every industry and has applications throughout many different value chains. Key areas for disruption are finance, insurance, healthcare, supply chains and digital identity. Governments, banks, and other large corporations are now getting behind both DLT and cryptoassets. Many established companies, ranging from Facebook to JP Morgan to Paypal, are now involved.

Footnotes

1 More on the “Austrian” view of Bitcoin in this article from one of our Economic advisors

https://en.aaro.capital/Article?ID=70eb25f1-32cc-4055-a602-0c9057a16d82

2 A more detailed explanation is provided in an article “Is Bitcoin Deflationary Money?”, written by one of our Economic advisors

https://en.aaro.capital/Article?ID=06dab68f-a232-472d-a811-0f2337d3c528

3 See for example the discussion in the Nobel prize Lecture of Christopher Sims "Statistical Modeling of

Monetary Policy and Its Effects", published in 2012 on the American Economic Review, 102 (4): 1187-1205.

4 For example, Bank of America commodity strategists note that “Looking year by year, we find that Bitcoin has been positively correlated with CPI inflation in 5 out of the 9 past years, with the largest correlations in 2014 and 2018. However when looking at correlations with inflation surprises since 2011, we find that Bitcoin has among the lowest co-movements, lagging most asset classes such as commodities, TIPS, and EM FX in particular.”

https://markets.businessinsider.com/news/stocks/bitcoin-price-today-inflation-hedge-portfolio-bank-of-america-price-2021-3

A broader discussion on the correlation of crypto assets and the equity market can be found in our article https://en.aaro.capital/Article?ID=503c42ba-df78-4037-b933-8713799b7cc9

5 Those interested can also look at our article, discussing the economics of “cryptocurrency as store of value”

https://en.aaro.capital/Article?ID=10a91479-ac4a-4945-afe7-fda07fd69f85

6 You can find more on this point in this short piece on “The Rise of Digital Monies”

https://en.aaro.capital/Article?ID=The%20Rise%20of%20Digital%20Money

7 Here you find more on “Currency Competition among National and Digital Monies”

https://en.aaro.capital/Article?ID=a54969cd-247a-4e0c-8a42-d454dd493979

8 We discuss whether “money is a public good” and the emergence of CBDCs in details in the following articles

https://en.aaro.capital/Article?ID=3981d31a-7f37-4efa-bb83-84a2ed054fb7

https://en.aaro.capital/Article?ID=62e63990-88a6-4163-8b16-5a0fc9de94bc

9 A detailed discussion on the “The Risk Landscape of Cryptoassets” and the emerging “Regulation in the Crypto Space” is provided here.

https://en.aaro.capital/Article?id=980bbf38-0ca7-49df-92fb-fc307edc4eb5

https://en.aaro.capital/Article?ID=984e2e3f-beac-4f44-8410-6896fe9e2620

Disclaimer